At the Cusp of a BaaS Revolution, Here Are Some of the Challenges

by Bosky S, Regional Head of BaaS, APAC, Finastra May 20, 2022The future of finance is open, and the rise of Banking-as-a-Service (BaaS) means this future is closer than ever.

The BaaS industry is quickly maturing, with 88% of senior APAC executives – in industries from banking and technology to healthcare and retail – recently telling Finastra that they are already implementing BaaS solutions or are planning to.

Financial institutions are evolving away from their traditional role as ‘closed shops’ and instead leveraging their banking licenses to integrate digital services directly into the products of consumer brands.

These consumer brands, or BaaS distributors, have identified the vast potential of distributing services such as buy-now-pay-later (BNPL) to consumers and corporate financing to businesses.

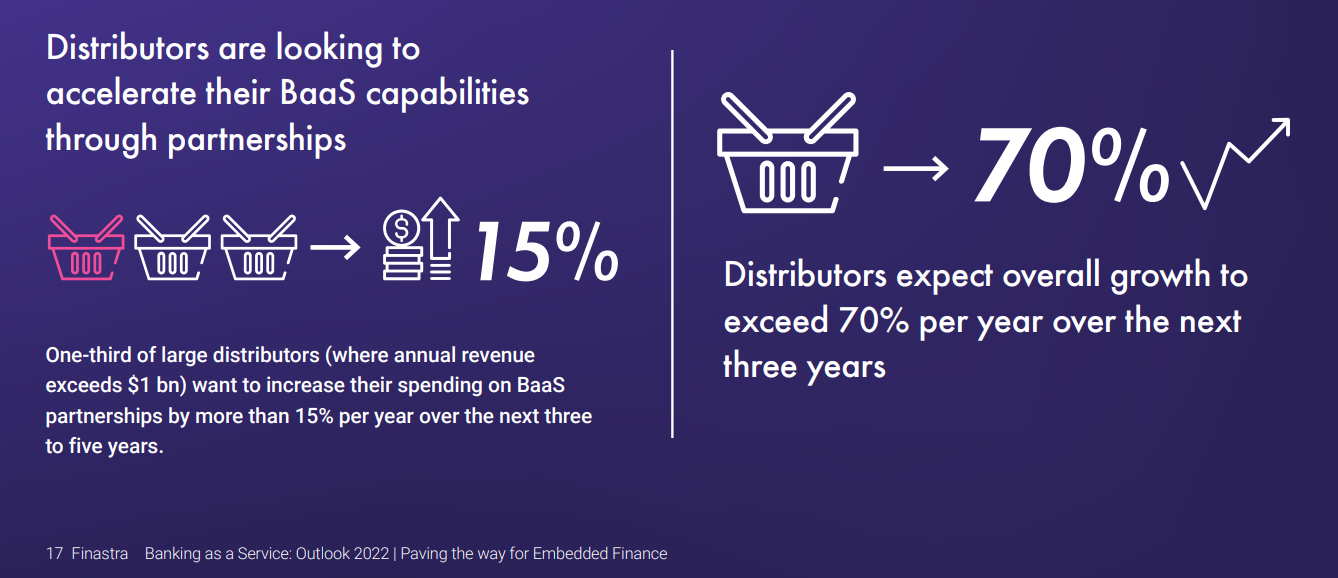

Finastra’s recent report, “Banking as a Service: Outlook 2022 | Paving the way for Embedded Finance” found that distributors expect overall growth to exceed a staggering 70% per annum over the next three years, with more than one third expecting to increase their revenues by more than 15% per year until 2024 by offering BaaS solutions.

There are, however, challenges ahead that need to be resolved if the BaaS industry is to reach its full potential.

For example, while distributors believe that a marketplace model will help retail and SME customers access the right product to cater their needs at better costs, they also have concerns around complexity – specifically regarding integration and regulation.

The key for distributors here will be to identify enablers, i.e. fintechs and bigtechs that help to embed financial services within distributors’ applications and platforms, that are mature enough to mitigate these issues for them.

It will also be important for distributors to consider partnerships that help them meet the needs of specific customers.

For example, corporate customers of enterprise resource planning (ERP) players require working capital loans that may need different features, pricing and terms for each sector, whereas customers of a retail chain may require BNPL and payment solutions.

The opportunity to customise offerings to highly targeted audiences is both an opportunity and a challenge of BaaS – but with the right enabler partnerships, distributors will be able to rise to this challenge and meet their customers’ needs seamlessly.

The second significant challenge distributors must resolve is that of user experience (UX). Creating a smooth and streamlined customer journey can be a time-consuming endeavour, but it’s worth it.

Many distributors already provide consumers with seamless payment experiences by offering different options like wallets, BNPL, and credit cards; but what about the needs of different types of customer?

For instance, a corporate customer will prefer a user experience that can integrate with their enterprise system, but a retail customer will favor a journey that is fast and easy to use.

Ultimately, the specific needs of a BaaS product’s target audience must be prioritised, alongside exceptional design and user interfaces.

Distributors are understandably keen to increase their customer stickiness, transaction volumes and average transaction values in order to drive increased revenues.

BaaS presents an opportunity to meet these goals without needing to obtain a banking license – a notoriously complicated, costly and time-consuming pursuit.

Furthermore, distributors typically enjoy the highest margins and maximum power in the BaaS value chain, thanks to their proximity to the end-customers. As such, their potential for growth in the space is unparalleled.

The key to maximising this opportunity will be carefully selecting the right partnerships and prioritising tailored customer journeys, enabling seamless experiences for all.

Access your copy of Finastra’s comprehensive market study of Banking-as-a-Service here.

{kind=link}